Kuflink mulls new BTL product suite as demand heats up

Copy the link below if the Read More link expires.

https://www.kuflink.com/wp-content/uploads/2021/09/Screenshot-2021-09-01-at-16.31.55.png

{kind=link}

Kuflink introduces instant bank transfers using open banking

Copy the link below if the Read More link expires.

Strong foundations

Copy the link below if the Read More link expires.

https://www.kuflink.com/wp-content/uploads/2021/08/Strong-foundations-_-Peer2Peer-Finance-News.pdf

Kuflink calls full time on partnership with Southampton FC

Copy the link below if the Read More link expires.

Kuflink’s New features for August 2021. Stand Up with CTO

The Kuflink Tech Team has worked diligently to bring new features for August 2021 forward. Together, with your feedback, we are able to fulfil Kuflink’s purpose in ‘Connecting People to Financial Freedom’.

Quote for August 2021

“Applied Faith: Faith is a state of mind through which your aims, desires, plans and purposes may be translated into their physical or financial equivalent.” – 3 of 17 Napoleon Hill’s 17 Principles of Success. (To see previous Napoleon Hill’s 17 Principles of Success please refer to previous CTO blogs).

What’s New or on its way to the Kuflink Platform & Kuflink Mobile APP for August 2021

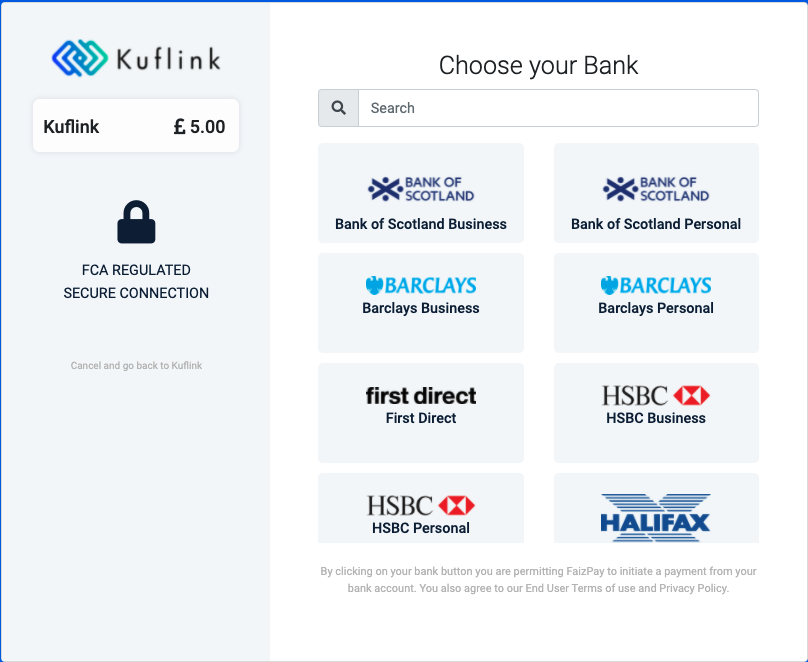

1) Released! A new “Instant Bank Transfer” payment facility using Open Banking via our approved FCA approved provider, FAIZPAY, is now live on the investment platform. This will allow users to transfer funds and update their e-wallets instantly. Learn more

2) Released! The feature to view select deals as a list is back after popular demand.

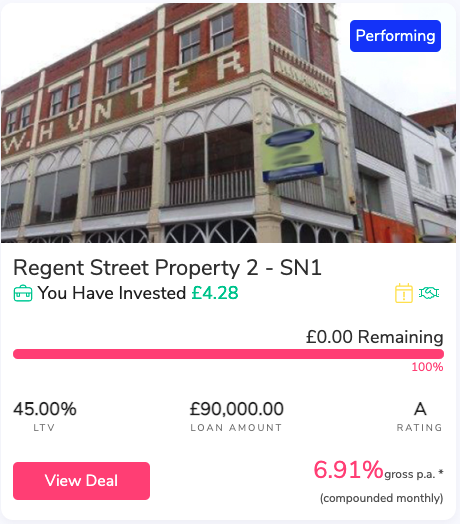

3) Released! The feature to show how much you have invested in Select deals has been made clearer.

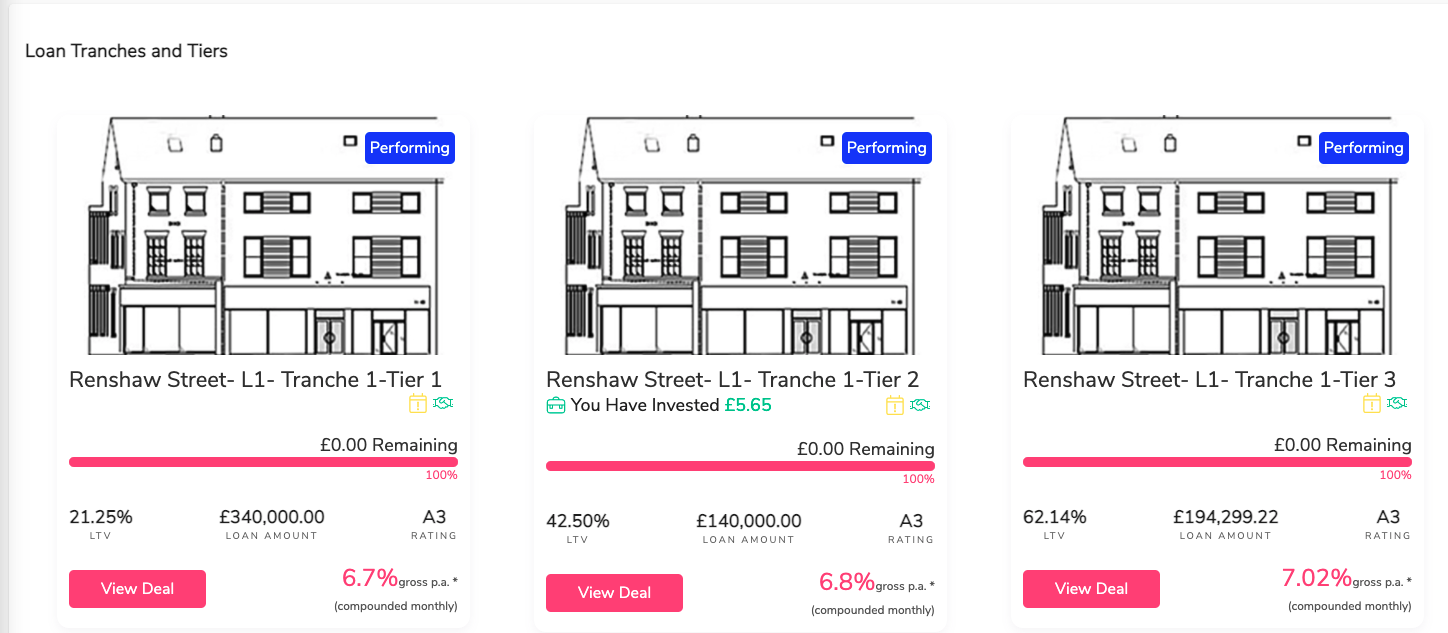

4) Released! The feature to show all other linked Tiers and Tranches in Select deals has now been introduced.

5) Released! You can now choose to compound the interest on your Auto-Invest and IF-ISA investments. Simply click the radio button when you choose how much, and for how long, to invest. Compounding can be a great way to maximise your returns.* At the end of each year, the interest you’ve accrued is reinvested – earning you interest on your interest!

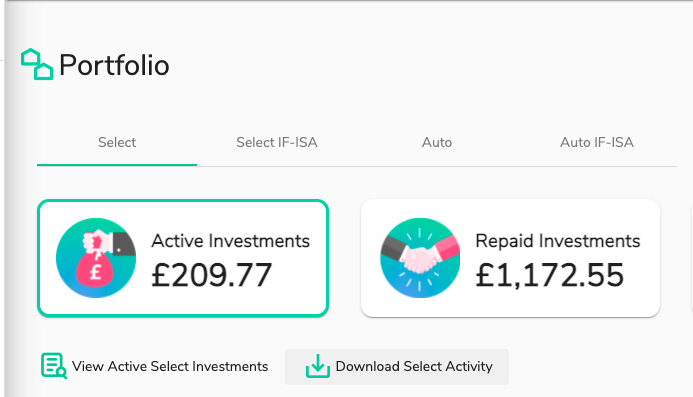

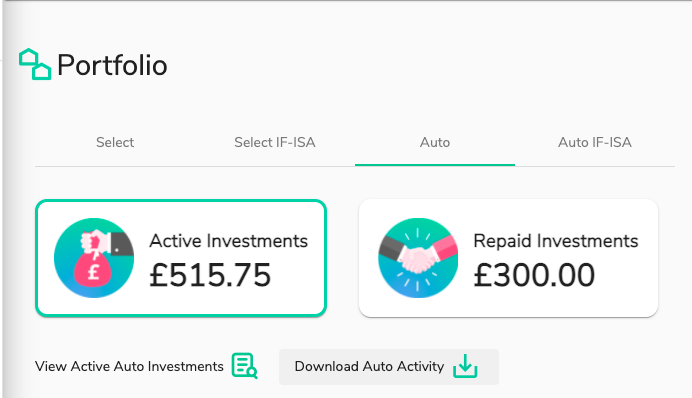

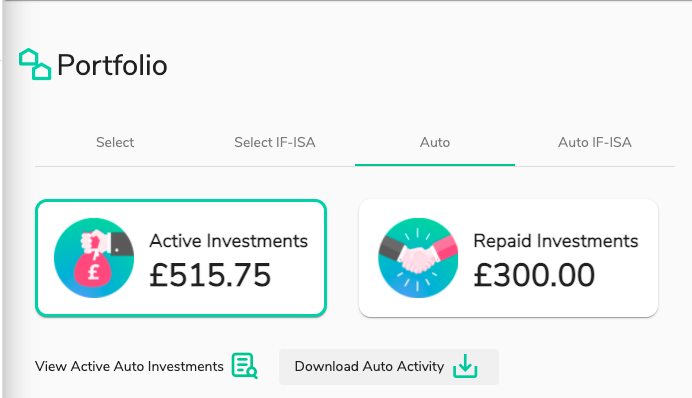

6) Released! You can now see a partial release of our new dashboard which shows you Select investments with or without an IF-ISA wrapper.

7) Released! You can now download a CSV showing you accrued interest in Select, Auto and IF-ISA Investments in the Portfolio section.

8) Released! Portfolio page show which Select Invest deals have been put into the ISA wrapper.

9) Coming Soon! We are now working on a new feature that will allow IF ISA Transfers In to enter into ISA eligible Select Invest Deals – this means clients can decide which ISA eligible Select Invest deals they want their ISA transfer to go into.

10) Coming Soon! A new segregated IF-ISA wallet, and SIPP wallet (which also comes with surprise features) – development has started.

11) Coming Soon! A new feature showing borrowers who have links as individuals, shareholders or directors, to other loans already on the platform is being built.

12) Coming Soon! A new feature showing where each development loan is in regards our new 7 phases of development – work has started.

13) Coming Soon! On the lending arm, we are currently building the process, through Open banking, to add an additional layer of borrower verification in real time and building a process to ascertain income vs expenditure for a potential borrower across all accounts. This is a step forward in reducing paperwork and unnecessary communication thereby improving efficiency in the process. All in all we should, in theory, gain access to all necessary information through a simplified online process as opposed to numerous phone calls, email chasers etc.

14) Coming Soon! Work on upgrading our proprietary deal risk / pricing tool in our CRM system by connecting to live data feeds, and allowing new fields to better assess the risk and price on deals is continuing. This is especially important in light of economic events like Brexit, the COVID-19 pandemic, and price hikes on raw materials (which will affect on-going Development appraisals). We are working with a ‘Royal Institution of Chartered Surveyors’ (‘RICS’) valuer and a seasoned developer / builder (both in our Credit committee), to further enhance the tool’s sensitivity to such events. We envisage connecting this information to our live loans on our platform to provide a timeline of any given loans risk.

15) Coming Soon! We are working on upgrading our Dashboard. Live Charts, proprietary budget tools, links to other investments, accrued interest, etc. will be on display in a singular view.

CTO thoughts for August 2021

As a Chief Technical Officer, I do not have all the answers, and this is ok. I used to put a lot of pressure on myself to solve everyone’s problems. However, I discovered this is not the best way, as the more problems I solved, the more problems I got, as people were looking for complete solutions from me. This is the route to burnout.

A true leader is one who asks for their team to present the problem and attempt to solve it themselves first. Discuss it on a stand up to get input from others, or in mini break out groups. Talk to other senior managers to ensure all areas are covered. Once this is done, only then can they discuss the problem with me to see if they are on the right path. Here the team member is growing and pushing themselves to learn and have the tools of a leader.

* Capital is at risk and Kuflink is not protected by the FSCS. Past returns should not be used as a guide to future performance. Securing investments against UK property does not guarantee that your investments will be repaid and returns may be delayed. Tax rules apply to IF ISAs and SIPPs and may be subject to change. Kuflink does not offer any financial or tax advice in relation to the investment opportunities that it promotes. Please read our risk statement for full details.

The 7 Phases of Development

Kuflink peer to peer lending has set up a development committee that reviews all the development projects every week. And when needed, we ask the borrowers to increase their equity in case we find that the costs are going beyond the original quote.

COVID-19 has affected almost every working sector. Therefore, it is no news that there has been an unexpected shortage of construction materials this year. Most people couldn’t have predicted the storm that has swept across the development sector. The UK government’s development goals are in jeopardy because of material shortage which has been caused mainly due to COVID-19 and Brexit.

Shortage in construction materials can also be traced back to the increased home improvement and building activities in 2020, specifically during the first lockdown across the UK. In addition, adjusting for the pandemic led to slow production of the construction materials from factories, and ever since, the supply chain has remained stretched.

Most developers have had to come up with creative methods to get around the additional customs paperwork, such as having to source more local materials. But, the fact remains the same that a lot of builders are dependent on imported materials.

Other than the domestic backlogs, there has also been a shortage of materials because of demand exceeding the labour supply. As a result, a few trades are hiking up their prices because of work overload. This condition is continuously constraining the production of specific products such as paints, adhesives and insulation, along with packaging for products, which is critical for developers.

There is also a shortage of lorry drivers reported by the Construction Leadership Council, which directly affects building sites receiving deliveries. There is a particular issue of transporters availability, and it is becoming a serious nationwide issue. This has caused extreme delays and has impacted a large number of project programmes.

How is the material shortage going to affect the UK developers and housebuilders?

If the material shortage continues to grow, it will be catastrophic for those working in construction with timber or steel frame. Both these materials are in short supply, which would lead to a rise in costs in the coming months. Developers undertaking refurbishment projects could also be affected by the increase in prices. The price of materials used for maintenance and repair work surged to 2% between March and April and rose by 11.2% between April 2020 and April 2021. In addition, building merchants are under immense pressure, which has left DIY projects in doubt, with sealants, paints and electrical parts being short in supply.

There are numerous key components for builders that are in high demand which can’t meet their volume of the order, like cement, steel, roof tiles, timber, plastics, plumbing items and plaster boards. Because of this high demand, low stock levels and long lead times, there is a surge in prices, especially with steel, paint, cement and timber.

Even with shortages, there is a way to navigate through this.

How to navigate through a material shortage in the 2nd half of the year?

· Plan in advance

Just like other construction projects, developers need to plan ahead. Planning in advance is the key, so you don’t get tangled in the mess of high prices and material shortages. There is an important point to keep in mind, especially over the summer when most people buy DIY and landscaping products, which places an additional burden on the supplies.

· Work with supply chain

You need to work closely with the supply chain. Also, you have to clearly communicate your requirements with the distributors, suppliers and builders’ merchants as early as possible.

The construction sector is growing and innovating with the use of modern construction techniques and factory building programmes. This is going to improve the production efficiency and quality. However, manufacturers will still be at the mercy of the market forces for construction material.

To sum it all up, the construction material shortage is becoming a serious and prolonged problem for UK’s developers and house builders. Therefore, as a lender, we have to be aware of the fact that the cost of development projects may change in the coming months. Also, we have to ensure that we are looking for ways to improve our lending criteria and offering to help developers with this situation.

Kuflink Property Development committee

Kuflink peer to peer lending has set up a property development committee that reviews all the development projects every week. Some of the members include our Head of Collections, Property Developers, a Builder, and a Royal Institution of Chartered Surveyor (RICS).

We also have an RICS build Appraisal calculator which uses the Building Cost Information Service (BCIS) database where we are able to use up-to-date benchmarking data to determine any adjustments needed based on current market conditions. And when needed, we ask the borrowers to increase their equity in case we find that the costs and or time are going beyond the original quote. Our committee identifies the progress of the development project using the ‘7 phases of development’ as mentioned below. See an actual example of a Development build that was funded by the Kuflink Peer to Peer platform.

.svg)

* Capital is at risk and Kuflink is not protected by the FSCS. Past returns should not be used as a guide to future performance. Securing investments against UK property does not guarantee that your investments will be repaid and returns may be delayed. Tax rules apply to IF ISAs and SIPPs and may be subject to change. Kuflink does not offer any financial or tax advice in relation to the investment opportunities that it promotes. Please read our risk statement for full details.